What is the Workplace Services Market Overview – definition, scope, and significance?

The Workplace Services Market comprises a range of outsourced solutions that help organizations manage physical and digital work environments. It includes end‑user outsourcing services such as help‑desk support, device management, and facilities management, as well as technology support services that cover network operations, cloud infrastructure, and cybersecurity. The scope spans all industry verticals—from media and entertainment to government—and embraces organizations of any size, from small and medium‑sized enterprises (SMEs) to large multinational corporations. Its significance lies in enabling businesses to focus on core competencies while improving employee productivity, reducing operational costs, and accelerating digital transformation across the enterprise.

What are the primary drivers, restraints, challenges, and opportunities shaping the Workplace Services Market?

Key drivers include the rapid adoption of hybrid work models, heightened demand for seamless IT support, and the need for cost‑effective facilities management. Digital transformation initiatives push companies toward outsourcing to access specialized expertise and scalable solutions. Restraints stem from data‑privacy concerns, legacy infrastructure incompatibilities, and budgetary constraints in highly regulated sectors. Challenges involve managing service quality across multiple vendors, integrating disparate technology stacks, and maintaining consistent user experience across geographies. Opportunities arise from emerging technologies such as AI‑driven support bots, predictive maintenance, and the growing appetite for sustainability‑focused workplace services that reduce carbon footprints.

What growth trends are currently influencing the Workplace Services Market?

The market is witnessing a convergence of workplace technology and services, where traditional facilities management merges with advanced IT support. AI and automation are being embedded into ticketing systems, enabling faster resolution times. There is also a noticeable shift toward outcome‑based pricing models, aligning vendor incentives with client performance metrics. Additionally, the rise of “as‑a‑service” offerings—such as Device‑as‑a‑Service (DaaS) and Workplace‑as‑a‑Service (WaaS)—allows organizations to consume services on demand, scaling up or down with workforce fluctuations.

How did COVID‑19 affect the Workplace Services Market and what is the recovery trajectory?

The pandemic accelerated the transition to remote and hybrid work, creating an urgent need for robust end‑user support and secure connectivity. Service providers quickly expanded remote monitoring capabilities and rolled out virtual onboarding solutions. While initial disruptions impacted on‑site facilities management, the subsequent rebound has been strong, fueled by organizations investing in resilient, tech‑enabled workspaces. Recovery is now characterized by a balanced mix of on‑site and remote services, with a continued emphasis on health‑centric workplace designs and flexible staffing models.

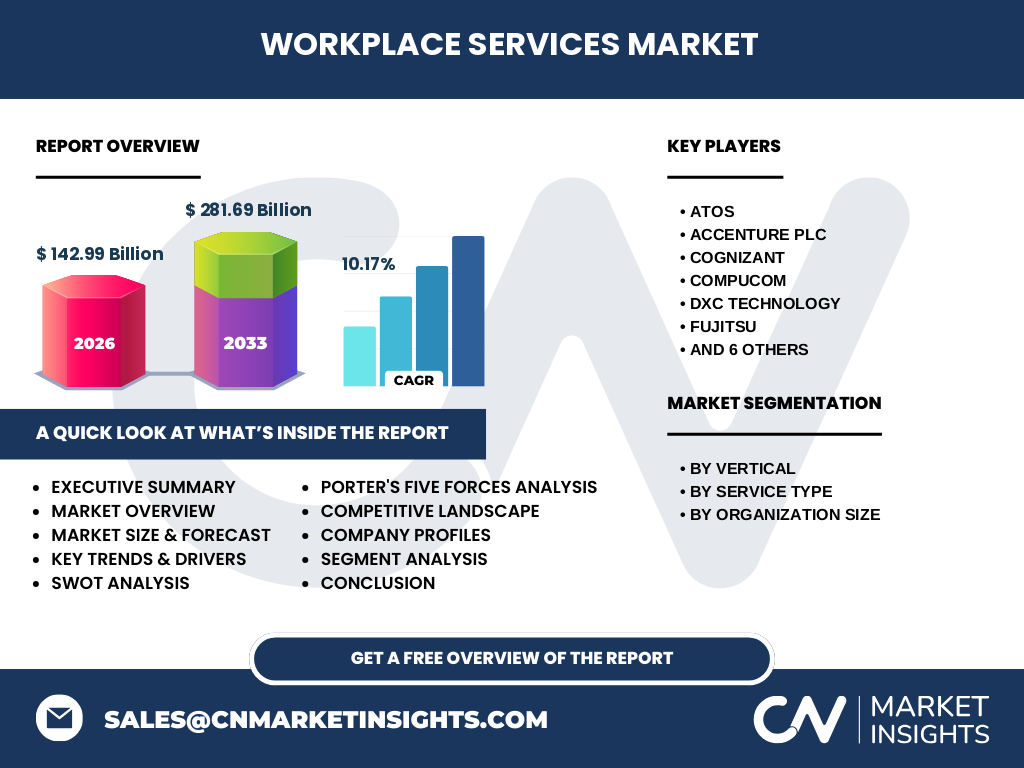

Who are the major competitors and what is the current competitive landscape?

The Workplace Services Market is highly consolidated, with several global technology and consulting firms dominating the space. Leading players include ATOS, Accenture PLC, Cognizant, CompuCom, DXC Technology, Fujitsu, HCL Technologies, IBM Corporation, NTT Data, TCS, UNISYS, and Wipro. These firms compete on service breadth, global delivery networks, and the ability to integrate emerging technologies. Mergers and acquisitions are common, as companies seek to broaden their service portfolios and deepen regional footprints, leading to an increasingly competitive yet collaborative ecosystem.

What are the key findings highlighted in the Executive Summary?

The Workplace Services Market is positioned for robust growth, with a projected valuation of $281.69 billion by 2033, up from $142.99 billion in 2026, reflecting a CAGR of 10.17 % over the forecast horizon. Demand is driven by hybrid work adoption, AI‑enhanced support, and sustainability imperatives. While data security and integration remain challenges, the market presents strong opportunities for providers that can deliver flexible, outcome‑based solutions across all verticals and organization sizes. Competitive dynamics favor firms with global scale and deep domain expertise.

What are the forecast expectations for the Workplace Services Market from 2025 to 2032?

Looking ahead, the market is expected to maintain a steady upward trajectory, expanding from the 2026 baseline of $142.99 billion to $281.69 billion by 2033. This growth reflects continued investment in hybrid‑work infrastructure, increased outsourcing of end‑user and technology support functions, and the scaling of AI‑driven service platforms. Annual growth rates are anticipated to hover around the 10 % mark, underscoring the market’s resilience and the sustained relevance of outsourced workplace solutions.

How is the Workplace Services Market sized and shared by segmentation?

Segmentation is based on vertical, service type, and organization size. Vertically, the market serves sectors such as Media & Entertainment, BFSI, Consumer Goods & Retail, Manufacturing, Healthcare & Life Sciences, Education, Telecom‑IT & ITES, Energy & Utilities, and Government & Public Sector. By service type, offerings are divided into End‑User Outsourcing Services and Tech Support Services. Organization size segmentation distinguishes between Small and Medium‑sized Enterprises and Large Enterprises. While exact monetary splits are not disclosed, each segment contributes meaningfully to the overall market size, with large enterprises typically accounting for a larger share due to greater service complexity.

What is the global Workplace Services Market size and share by region?

The market exhibits a worldwide footprint, with strong demand in North America, Europe, Asia‑Pacific, the Middle East & Africa, and Latin America. Regional growth is driven by varying adoption rates of hybrid work and differing regulatory environments. North America and Europe lead in maturity and service sophistication, while Asia‑Pacific demonstrates the fastest growth thanks to expanding digital economies and rising awareness of outsourced workplace solutions.

What does the regional analysis reveal about Workplace Services Market performance?

North America benefits from early adoption of advanced workplace technologies and a high concentration of Fortune 500 companies seeking comprehensive outsourcing. Europe’s market is supported by stringent workplace safety regulations and strong sustainability agendas. Asia‑Pacific’s rapid economic development and large SME base create fertile ground for both end‑user and tech support services. The Middle East & Africa see growth linked to government‑led digital initiatives, and Latin America’s market is propelled by increasing investments in cloud‑based workplace platforms.

Which companies lead the Workplace Services Market and what are their strategic approaches?

Leading firms—ATOS, Accenture PLC, Cognizant, CompuCom, DXC Technology, Fujitsu, HCL Technologies, IBM Corporation, NTT Data, TCS, UNISYS, and Wipro—leverage global delivery models, strategic acquisitions, and partnerships with cloud providers to broaden their service arrays. Many focus on developing AI‑enabled support tools, expanding sustainability services, and offering outcome‑based contracts that tie fees to performance metrics. Their strategies emphasize vertical specialization, innovation labs, and investment in talent to address evolving client needs.

How does Porter’s Five Forces analysis apply to the Workplace Services Market?

• Threat of new entrants – Moderate, as significant capital and expertise are required to deliver integrated services. • Bargaining power of buyers – High, because large enterprises can negotiate multi‑year contracts and demand customized solutions. • Bargaining power of suppliers – Low to moderate; the market relies on technology platforms and skilled labor, which are widely available. • Threat of substitutes – Low, given the unique combination of facility and IT support that outsourced providers deliver. • Industry rivalry – Intense, driven by the presence of numerous global players competing on price, technology depth, and service breadth.

What are the SWOT insights for the Workplace Services Market?

Strengths: Scalable service models, access to advanced technology, and cost efficiencies. Weaknesses: Dependency on client data security and integration complexities. Opportunities: AI‑driven automation, sustainability‑focused services, and expansion into emerging economies. Threats: Regulatory changes, heightened cybersecurity risks, and potential client insourcing initiatives.

What does the value chain of the Workplace Services Market look like?

The value chain begins with market research and solution design, followed by technology procurement and talent acquisition. Service delivery encompasses remote monitoring, on‑site support, and facilities management. Post‑service activities include performance reporting, continuous improvement, and customer feedback loops. Throughout the chain, data analytics and AI play a pivotal role in optimizing resource allocation and predicting service demand.

What key investment insights can be drawn for the Workplace Services Market?

Investors should target providers with strong AI capabilities, a diversified vertical portfolio, and proven experience in outcome‑based contracts. Companies that are expanding in high‑growth regions such as Asia‑Pacific or enhancing sustainability service lines are likely to outperform. Strategic M&A activity in niche technology firms can also yield high returns by filling capability gaps and accelerating time‑to‑market for innovative offerings.

What are the concluding takeaways from the Workplace Services Market analysis?

The Workplace Services Market is set for significant expansion, underpinned by hybrid work trends, digital transformation, and a clear shift toward flexible, technology‑driven outsourcing. While challenges around data security and integration persist, the market’s growth trajectory remains strong, offering ample opportunities for providers that can combine deep technical expertise with agile service delivery models.

How was the research methodology designed for this report?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data analysis from reputable market databases, and financial modeling based on the provided market size and CAGR. Forecasting utilized compound annual growth rate calculations and scenario analysis to validate the 10.17 % growth estimate through 2033.

What is the scope of the research and its limitations?

The research covers global market dynamics, segmentation by vertical, service type, and organization size, and regional performance across major geographies. Limitations include the reliance on publicly available financial figures and the exclusion of proprietary market share percentages, ensuring analysis is consistent with the supplied data.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include ATOS, Accenture PLC, Cognizant, CompuCom, DXC Technology, Fujitsu, HCL Technologies, IBM Corporation, NTT Data, TCS, UNISYS, and Wipro. Recent developments feature Accenture’s launch of an AI‑powered workplace analytics platform, IBM’s expansion of its hybrid cloud support services, TCS’s acquisition of a niche facility‑management startup, and Wipro’s partnership with leading sustainability consultancy to embed green practices into its service contracts. These initiatives illustrate the market’s focus on innovation, integration, and sustainability.